In case of an eventuality, nominee is the beneficiary and supersedes the Will for PPF and Life Insurance

This is an important aspect of financial planning to ease the process of transfer of your assets - liquid or otherwise - in case of your death. It will ensure that, in your absence, your family can access the wealth without too much of an hassle.

Nominee or Will

At the time of opening a bank account, buying a life insurance policy or residential property, it is essential to mention a nominee. It could be your wife, children, mother, father, brother, sister or uncle. In case of your death, the nominee will easily get these assets.

However, the nominee is not the rightful or legal owner of the money in your bank account or of your assets. But under Companies Act, a nominee mentioned in equity shares held in demat account can be a legal heir.

Sachin Parekh, founder Save N Protect Financial Planners, says an individual may have multiple assets such as mutual funds, fixed deposits and insurance policies. "Not doing proper nomination and succession planning can put the individual at the risk of losing the assets completely or the nominees going through lot of trouble to recover them."

According to Karan Gupta of Sykes and Ray Equities, a Will and a nominee appointment should be in sync. The nominee is the ultimate owner only in two cases, where the nominee is the beneficiary and supersedes the Will. One: under Life Insurance (Married Women's Property) Act, 1874, and two, in Public Provident Fund.

"In case of demat account if the value of the fund is more than Rs 5 lakh then probate is needed," Gupta said.

A probate is a process under law where the Will of a person is scrutinised for its authenticity.

Nominee can give a valid discharge

Harshvardhan Roongta, of Roongta Securities, says a nominee can give a "valid discharge" for the bank, a company or any other financial institution that wants to settle the 'liability'. Say, for example, if a policyholder appoints a nominee, then the liability of the insurance company with respect to the policy stands discharged, when the amount is paid to the registered nominee.

"Whether there is a dispute in a family over succession of assets or not, one should make a Will, as it is helpful in smooth transfer of one's assets to the next generation," Roongta says.

If a person makes his or her brother a nominee in a property or a flat, the brother becomes a nominee transferee. He is not a proper or permanent transferee and can only deal with aspects like clearing dues of the society and taking care of the property. "He becomes a nominee member with no further rights to sell or transfer the property under the Cooperative Societies Act," Roongta explains.

Harshvardhan Roongta, of Roongta Securities, says a nominee can give a "valid discharge" for the bank, a company or any other financial institution that wants to settle the 'liability'. Say, for example, if a policyholder appoints a nominee, then the liability of the insurance company with respect to the policy stands discharged, when the amount is paid to the registered nominee.

"Whether there is a dispute in a family over succession of assets or not, one should make a Will, as it is helpful in smooth transfer of one's assets to the next generation," Roongta says.

If a person makes his or her brother a nominee in a property or a flat, the brother becomes a nominee transferee. He is not a proper or permanent transferee and can only deal with aspects like clearing dues of the society and taking care of the property. "He becomes a nominee member with no further rights to sell or transfer the property under the Cooperative Societies Act," Roongta explains.

Anyone can make a Will

Don't rely on a nominee alone. Draw up a Will which will prevail in most circumstances. A Will is a document that clarifies a lot of things. "A Will is has got nothing to do with the amount of money or the number of assets involved that a person wants to transfer," says Suresh Sadagopan, founder, Ladder7 Financial Advisories.

When one appoints a nominee he or she should also make the same person a beneficiary. "A nominee and a beneficiary should always be the same person. In case of a married couple, the natural beneficiary will be the spouse," Sadagopan adds. If a person dies interstate, according to the Hindu Succession Act, assets will go to the legal heir and follow a trajectory before they go to the lawful owner. "If a person had made a Will, then after his death the assets will go to the person who is named in the Will. It must be noted that ancestral properties cannot be willed under Hindu Succession Act," Sadagopan points out.

Wife natural beneficiary of joint account

In case of a joint bank account, when the husband dies, the wife becomes natural beneficiary. The bank may ask for succession certificate. The Will is probated and the death certificate also sought in certain cases. If there is no Will, the deceased's children, mother or siblings can issue a no-objection certificate allowing the deceased's wife to lay claim over his assets.

FOR SMOOTH TRANSFER OF ASSETS

Give power of attorney (PoA) on incapacity, in case the person is mentally ill or incapacitated to take sane decisions, two doctors need to certify

In case of a non-Muslim and two marriages, it is mandatory for one marriage to be void. Even though marriage is void, children born out of a marriage with a ceremony have a stake in the inheritance

All adults should have a durable PoA, specific PoA in case of incapacity

Don't rely on a nominee alone. Draw up a Will which will prevail in most circumstances. A Will is a document that clarifies a lot of things. "A Will is has got nothing to do with the amount of money or the number of assets involved that a person wants to transfer," says Suresh Sadagopan, founder, Ladder7 Financial Advisories.

When one appoints a nominee he or she should also make the same person a beneficiary. "A nominee and a beneficiary should always be the same person. In case of a married couple, the natural beneficiary will be the spouse," Sadagopan adds. If a person dies interstate, according to the Hindu Succession Act, assets will go to the legal heir and follow a trajectory before they go to the lawful owner. "If a person had made a Will, then after his death the assets will go to the person who is named in the Will. It must be noted that ancestral properties cannot be willed under Hindu Succession Act," Sadagopan points out.

Wife natural beneficiary of joint account

In case of a joint bank account, when the husband dies, the wife becomes natural beneficiary. The bank may ask for succession certificate. The Will is probated and the death certificate also sought in certain cases. If there is no Will, the deceased's children, mother or siblings can issue a no-objection certificate allowing the deceased's wife to lay claim over his assets.

FOR SMOOTH TRANSFER OF ASSETS

Give power of attorney (PoA) on incapacity, in case the person is mentally ill or incapacitated to take sane decisions, two doctors need to certify

In case of a non-Muslim and two marriages, it is mandatory for one marriage to be void. Even though marriage is void, children born out of a marriage with a ceremony have a stake in the inheritance

All adults should have a durable PoA, specific PoA in case of incapacity

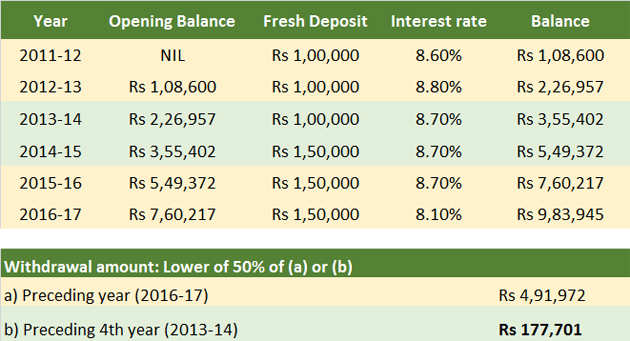

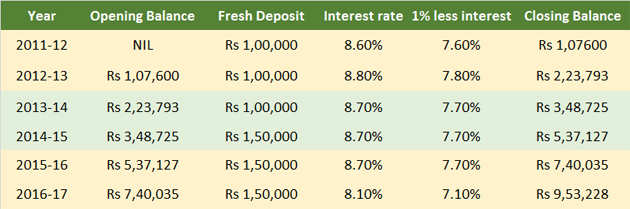

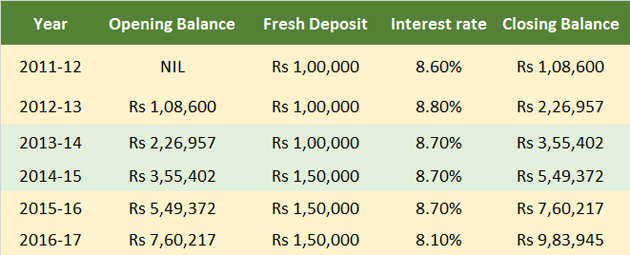

Source: Sykes & Ray Equities